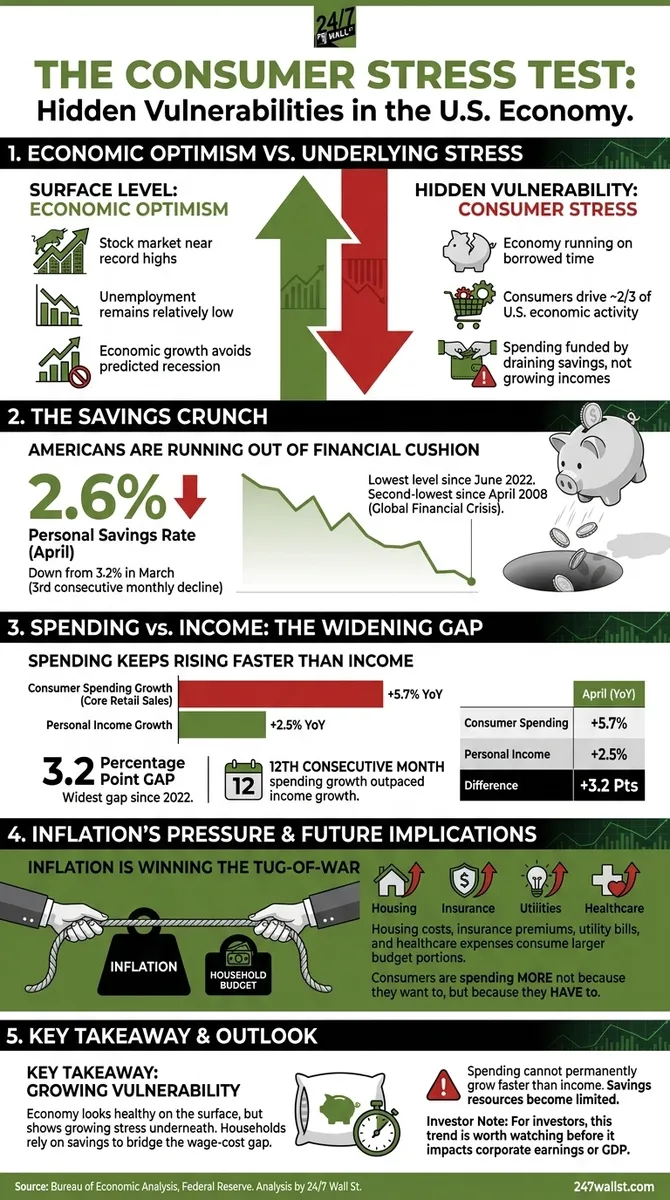

While the stock market approaches record highs and unemployment remains low, signaling a potentially robust economy, a critical underlying vulnerability is emerging. The American consumer, the primary engine of U.S. economic activity, appears to be sustaining current spending levels by depleting savings rather than through increased income. This trend, if continued, presents a significant risk to the long-term economic outlook.

Recent data from the Bureau of Economic Analysis (BEA) and the Federal Reserve indicates a concerning decline in the personal savings rate. This shift suggests that households are increasingly reliant on their financial cushions to cover expenses, a strategy that is inherently unsustainable and leaves them exposed to economic shocks. The implications are particularly significant for economic policies reliant on sustained consumer spending.

Declining Personal Savings Rate Signals Financial Strain

The U.S. personal savings rate has seen a notable decrease, dropping to 2.6% in April, according to the BEA's Personal Income and Outlays report. This figure represents a decline from 3.2% in March and marks the third consecutive monthly decrease. Over this three-month period, the savings rate has contracted by a cumulative 1.7 percentage points.

Historical data from the Federal Reserve highlights that April's 2.6% savings rate is the lowest recorded since June 2022. It also stands as the second-lowest rate observed since April 2008, a period marked by the global financial crisis. This precipitous drop indicates that American households are spending a significantly larger portion of their earnings, leaving minimal reserves for unexpected expenditures such as job losses, medical emergencies, or other unforeseen economic challenges.

This financial tightening is further exacerbated when juxtaposed with personal income growth. In April, consumer spending, specifically within core retail sales, rose by 5.7% year-over-year. In stark contrast, personal income saw a more modest increase of 2.5% over the same period. This creates a widening gap of 3.2 percentage points, the largest disparity observed since 2022.

This trend of spending outpacing income has persisted for twelve consecutive months, a sustained period that underscores a growing reliance on drawing down existing savings. While consumers can temporarily bridge this gap using savings, credit, or home equity, these resources are finite. The economic model is predicated on spending growing in line with, or influenced by, income, not consistently exceeding it without a corresponding income increase.

Inflationary Pressures Driving Consumption Patterns

The current economic climate suggests that consumers are not necessarily spending more out of increased confidence, but rather out of necessity to maintain their existing standard of living. Persistent inflation across various sectors is a significant contributing factor.

Elevated housing costs, soaring insurance premiums, rising utility bills, and increased healthcare expenses are collectively consuming a larger share of household budgets. This dynamic forces consumers to allocate more of their income towards essential goods and services, leaving less for discretionary purchases. Consequently, consumer spending is driven by the need to cover rising costs rather than an expansion of purchasing power.

Impact Analysis

The sustained divergence between consumer spending and income growth, coupled with a critically low savings rate, points to a significant economic vulnerability. While consumer spending currently supports economic activity, its foundation is increasingly precarious. A sharp decline in savings leaves households susceptible to economic downturns, potentially leading to a significant contraction in discretionary spending. This could have a cascading effect on consumer-facing businesses, impacting corporate earnings and overall GDP growth. The sustainability of the current economic performance is therefore highly dependent on future income growth catching up to or exceeding expenditure, or a significant reduction in inflationary pressures.