Adobe, a long-standing titan in the software industry, has experienced a significant market correction, shedding 27.61% year-to-date. This sharp decline, however, presents a compelling investment opportunity according to proprietary market analysis. Despite the recent downturn, the stock is trading substantially below its fundamental valuation, suggesting a potential for robust recovery.

The current market sentiment appears to have overlooked Adobe's consistent performance, particularly its ability to surpass earnings expectations for four consecutive quarters. This disconnect between performance and stock price indicates a potential market overreaction, creating a favorable entry point for investors anticipating a return to intrinsic value.

Adobe's Market Performance and Valuation

Once trading at over $400 per share, Adobe's stock has fallen to approximately $253.37, marking a 39.33% decrease over the past year and a 22% drop from its 52-week high. This depreciation occurred even as the company reported strong financial results, including a 12.0% year-over-year revenue increase to $6.40 billion and non-GAAP EPS of $6.06 in its Q1 FY2026 earnings report. The market's negative reaction to these results was reportedly influenced by the CEO's upcoming transition and ongoing narratives surrounding AI competition and acquisition strategies, such as the pending Semrush deal.

Despite these headwinds, recent trading shows a positive uptick, with Adobe's stock gaining 7.33% in the past week. This suggests a potential shift in market sentiment, possibly driven by a reassessment of the company's underlying value and future prospects.

Proprietary Model Projections for Adobe

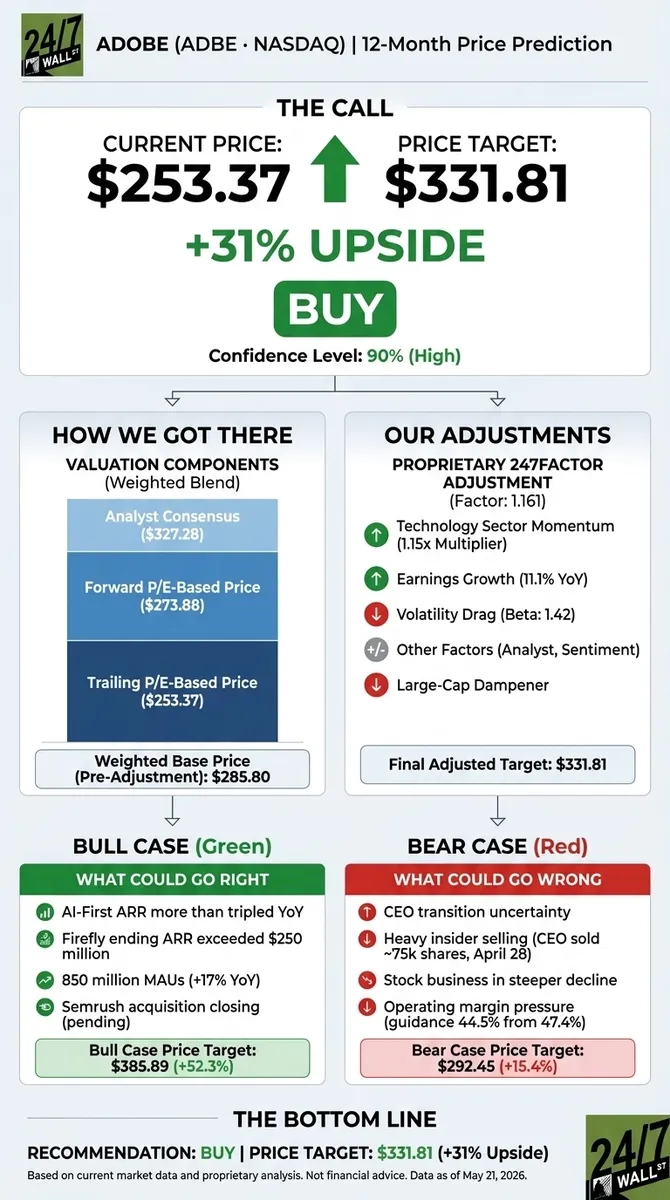

A detailed analysis using a proprietary valuation model indicates a target price of $331.81 for Adobe over the next 12 months. This projection is derived from a blend of valuation anchors, including trailing and forward P/E ratios, as well as analyst consensus targets. The model suggests an upside potential of approximately 31% from current trading levels, with a high confidence reading of 90%.

The model integrates multiple valuation methodologies to provide a comprehensive outlook. The trailing P/E ratio suggests a target price of $253.37, the forward P/E points to $273.88, and the consensus analyst target stands at $327.28. When weighted, these figures yield a pre-adjustment value of $285.80, reinforcing the notion that the stock is currently undervalued by the market.

Bullish Case: AI Monetization and Ecosystem Growth

The optimistic scenario for Adobe's stock anticipates a rebound to $385.89, representing a total return of 52.3%. This projection is primarily driven by the company's successful monetization of its artificial intelligence initiatives. Adobe's AI-first Annual Recurring Revenue (ARR) has more than tripled year-over-year, with Firefly's ARR exceeding $250 million. Furthermore, the Adobe ecosystem continues to expand, boasting 850 million monthly active users, a 17% year-over-year increase.

With a forward P/E ratio of just 11 and a PEG ratio of 0.724, the current valuation appears exceptionally attractive, suggesting significant multiple compression has already occurred. The acquisition of Semrush, expected to close in Q2, is anticipated to enhance brand visibility capabilities, a factor not yet fully incorporated into current financial guidance. Of the 39 analysts covering Adobe, a significant portion rates the stock as a Buy or Strong Buy, with a consensus target price of $327.28.

Bearish Scenario and Downside Risks

Conversely, the bearish outlook from the proprietary model targets a price of $292.45, which still remains above the current trading price. However, the most substantial downside risks are centered on execution challenges and strategic uncertainties. The unresolved CEO succession plan introduces a layer of strategic ambiguity. Additionally, insider trading activity has shown a notable trend of selling, with the outgoing CEO, Shantanu Narayen, selling approximately 75,000 shares in late April.

The decline in Adobe's stock photography business, a segment valued at roughly $450 million, is steeper than initially projected, exacerbated by the competitive pressure from generative AI technologies. Guidance for Q2 suggests a potential dip in non-GAAP operating margins to 44.5% from 47.4%. Bulls, however, argue that this margin compression is a deliberate strategic move to reinvest in AI-driven products like Firefly and GenStudio, as well as freemium models, which are expected to bolster long-term ARR growth despite short-term impacts.

Risk/Reward Profile and Future Outlook

Considering Adobe's current valuation at 11x forward earnings, a 29.5% profit margin, a 58.8% return on equity, and the impressive tripling of AI-first ARR, the market appears to have overcorrected. The 24/7 Wall St. price target of $331.81 remains a strong Buy recommendation, supported by 90% confidence. The primary driver for this bullish stance is Adobe's potential to convert its vast user base of 850 million monthly active users into paying subscribers over the next 18 months.

The counterarguments focus on the potential for strategic drift during the CEO transition and the possibility of AI-native competitors capturing the small and medium-sized business (SMB) creative market more rapidly than Adobe can counter. Nevertheless, the current valuation reset has seemingly mitigated much of the downside risk, presenting an attractive risk/reward proposition for prospective investors.

Adobe Price Projections: 2026-2030

Future price targets for Adobe are projected based on an assumed annualized base-case return of approximately 16.7%, aligning with the company's five-year model trajectory. These projections anticipate a sustained growth path, though significant upward or downward deviations could occur based on several key factors. The successful integration of the Semrush acquisition, the clarity and strategic direction set by the new CEO, and the competitive landscape shaped by AI advancements from major players like OpenAI, Google, and Microsoft will be critical determinants of Adobe's future stock performance.